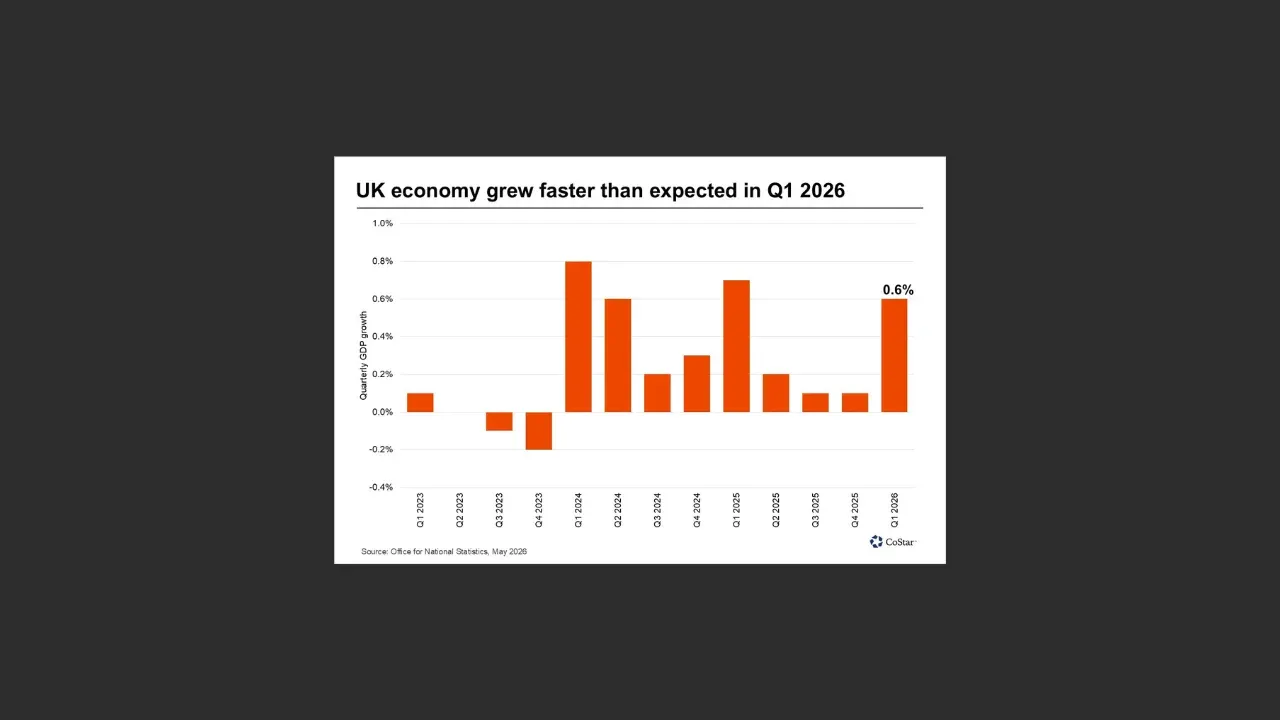

CoStar’s latest UK economic snapshot shows a 0.6 % quarterly expansion in Q1 2026, up from a modest 0.1 % in the final quarter of 2025. The data, released by the commercial‑real‑estate analytics firm, highlights a services‑led recovery, modest construction rebound, and a lingering weakness in travel‑related activity. For banks, lenders, and compliance teams, the numbers reshape short‑term credit‑risk models and reporting expectations.

Services‑Driven Momentum and Sectoral Shifts

The services sector anchored the quarterly gain, with the PMI indicating a steady expansion at 52.7. Manufacturing output rose to a near four‑year high, reflected in an April PMI of 53.6. Construction posted a 0.4 % increase, but the growth stemmed primarily from repair and maintenance work rather than new builds. Production output, which includes manufacturing, edged up 0.2 %.

Conversely, travel agencies and tour operators dragged on GDP, posting a 6.4 % month‑over‑month decline. This sectoral divergence suggests that while consumer‑facing services are rebounding, discretionary travel remains vulnerable to lingering pandemic‑related constraints and cost pressures.

Credit‑Risk Implications for Lenders and Investors

Financial institutions that underwrite commercial real estate loans must reassess exposure to construction projects. The shift toward refurbishment indicates a lower risk of over‑leveraged new‑development pipelines, but also signals tighter margins for developers reliant on new‑build pipelines.

Banks with SME loan books in the services arena may see improved repayment capacity, given the PMI‑derived expansion. However, the pronounced dip in travel‑related activity raises red flags for lenders with exposure to hospitality and tourism operators. Risk models should incorporate the 6.4 % contraction as a stress‑scenario parameter for the next two quarters.

Compliance, Disclosure, and Regulatory Reporting

The UK’s Prudential Regulation Authority (PRA) expects firms to reflect macro‑economic shifts in their stress‑testing frameworks. The CoStar data provides a granular view that can be used to calibrate scenario analyses, especially for sectors with divergent trajectories.

Moreover, the upcoming Corporate Governance Code revisions emphasize transparent disclosure of sector‑specific risks. Institutions should consider augmenting their ESG reports with metrics on service‑sector resilience versus travel‑sector exposure, aligning with the regulator’s focus on material financial‑risk drivers.

Strategic Outlook for Market Participants

The modest but broad‑based growth suggests a “soft‑landing” narrative, yet the uneven sector performance warrants caution. Asset managers may tilt allocations toward service‑heavy equities and away from travel‑linked securities until the latter shows a sustained recovery.

Policy makers, meanwhile, could target fiscal incentives to stimulate new‑build construction, balancing the current repair‑focused activity. Such measures would diversify the construction pipeline and mitigate concentration risk in the refurbishment niche.

Key Takeaways

- UK Q1 2026 GDP grew 0.6 % YoY, driven by services (PMI 52.7) and modest manufacturing (PMI 53.6).

- Construction rose 0.4 % mainly from repair/maintenance; new‑build activity remains subdued.

- Travel agency and tour‑operator output fell 6.4 % month‑over‑month, highlighting sectoral weakness.

- Lenders should adjust credit‑risk models to reflect stronger service‑sector borrowers and heightened travel‑sector stress.

- Compliance teams need to embed these macro trends into stress‑testing and ESG disclosures per PRA expectations.

FinanceInsyte's Take

CoStar’s data confirms that the UK economy is outpacing short‑term expectations, but the uneven recovery across sectors introduces nuanced risk considerations. Financial institutions that integrate these granular insights into credit assessments, regulatory reporting, and strategic planning will be better positioned to navigate the evolving landscape. Ongoing monitoring of services momentum and travel‑sector rebound will be essential for maintaining resilient portfolios and meeting compliance obligations.

Source: Businesswire